The Corporate Treasury Function

The treasury function in corporate finance is the operational function responsible for a firm’s cash, funding, and financial risk: keeping the firm liquid, financing its obligations, moving money between accounts and legal entities, and managing the currency, interest-rate, and counterparty exposures that sit on the balance sheet as a by-product of operating. Treasury owns the cash position, the bank relationships and account architecture through which cash moves, access to short- and long-term funding, and the controls over how money leaves the firm. In a mid-to-large corporate this work sits in a dedicated function under a group treasurer; in a smaller firm it is a cluster of responsibilities held by a controller or CFO — the reporting line differs, the work is the same.

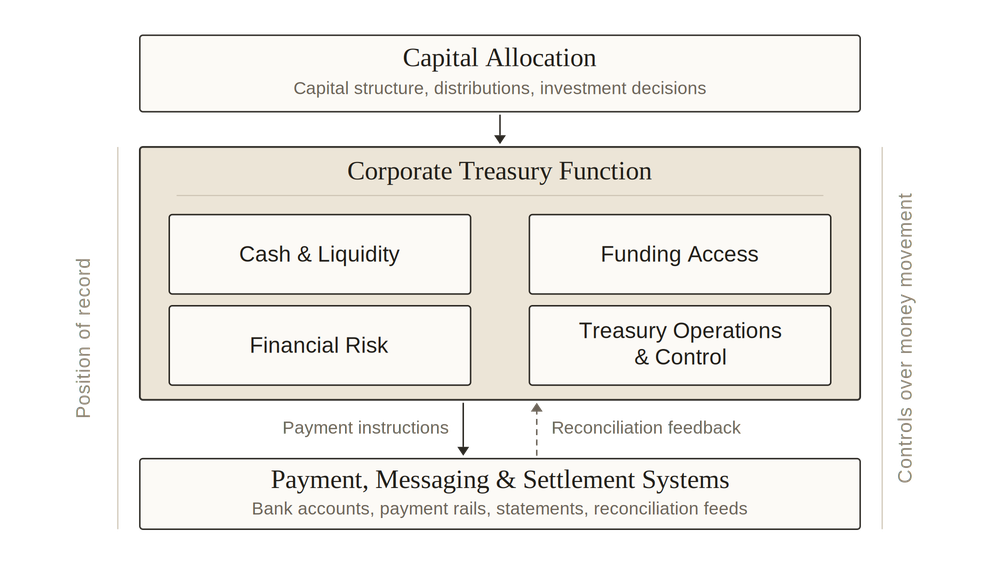

The function sits between two layers it does not own. Above it is capital allocation — how much capital the firm holds and where it is deployed; treasury executes against that decision and keeps the firm solvent and liquid while the decision plays out, without making the decision itself. Below it are the payment, messaging, and settlement systems that move individual transactions; treasury sets the account structure and connectivity through which those transactions route and reconcile, but the per-instruction mechanics belong to the rails. What treasury holds is the operating layer in between — the positions, structures, and controls that determine whether the firm can pay what it owes, when and in the currency it owes it, without tying up more cash or carrying more risk than intended.

Scope and Boundary of the Treasury Function

Where the treasury function ends and the next function begins is a question of ownership: cash, transactions, forecasts, and risk are objects treasury shares with the functions on either side of it, and the boundary is wherever ownership of one of those objects is assigned. Three questions settle it in practice — who holds the cash position of record, who initiates and who reconciles a movement of money, and who carries which forecast. Draw the lines cleanly and each object has one owner and a defined hand-off to the next function. Draw them poorly and the failure is predictable: two functions each assume the other reconciles the bank account, or two cash figures built on different data diverge and the firm cannot say which one is correct.

Treasury, Accounting, and FP&A

These three functions touch cash at different points and to different ends.

| Function | Owns | Cash figure | Horizon |

|---|---|---|---|

| Accounting | General ledger, books of record, period close | Booked balance reconciled to the bank statement (ISO 20022 camt.053), as of a closed period | Historical, closed |

| Treasury | Cash position, bank relationships, account architecture, payment release | Live intraday position from same-day statements (camt.052) and known inbound/outbound flows | Today plus near-term forecast |

| FP&A | Budget, operating plan, earnings forecast | Derived from the operating plan, not read off bank balances | Longer-horizon plan |

Two operational seams run between these views. The first reconciles accounting’s booked cash against treasury’s managed cash: the two should tie out, but they are built from different feeds and different as-of points, so the discipline of reconciling them is where breaks surface — a payment treasury released that accounting has not yet booked, a bank fee accounting recorded that treasury never forecast. The second runs between FP&A’s plan-driven cash view and treasury’s flow-driven short-term forecast — different horizons, different granularity — and unless the two reconcile at the boundary the firm carries two numbers that disagree about the same future.

Harder than either seam is the boundary of authority. Payment release and bank-account ownership sit with treasury; accounting records the resulting entry — the two roles held apart so that no single function both moves money and books it. Let the separation erode, with accounting staff granted release rights or treasury cutting ledger entries, and segregation of duties fails, taking the control surface that catches fraud and error down with it.

Treasury and Capital Allocation

Upward, the boundary runs between treasury and capital allocation. Allocation decides how much capital the firm holds, the target capital structure, distribution policy, and which investments and acquisitions get funded — board- and CFO-level calls about where capital goes. Against those decisions treasury executes, and holds the firm in the condition they require: it raises the funding an allocation decision calls for (drawing the revolver, issuing commercial paper, running the mechanics of a bond issue), keeps the firm liquid while capital is committed, manages the interest-rate and currency risk the capital structure creates, and supplies the information the decision runs on — liquidity position, funding capacity, the cost of available capital, covenant headroom.

What treasury does not do is set the leverage target, declare the dividend, or choose which acquisition to fund. It reports what is feasible and at what cost, then executes the chosen path. The relationship runs both ways at the edges: a thin liquidity position or exhausted funding capacity narrows what is deployable, and the price and availability of capital feed back into the decision — but the decision itself belongs to allocation. Covenants make this concrete. A funding decision creates covenant tests — leverage, interest coverage, minimum liquidity — and treasury monitors headroom and flags when a contemplated action would breach one; whether to take the action, and whether to seek a waiver, sits above the function. Treasury owns the measurement and the warning; allocation owns the call. When that split slips — treasury blocking a board-sanctioned draw, or allocation committing to a deal treasury has flagged as unfundable — the firm pays for it directly, in deployable capital left on the table or a covenant tripped on a draw that should never have cleared.

The Treasury Mandate

Four domains of responsibility make up the treasury mandate. Three of them concern a condition the firm needs held — liquidity, funding, and financial risk kept within tolerance — and the fourth is the operational apparatus that executes and verifies the work of the other three. Their edges overlap by design: funding capacity backstops liquidity, financial risk arises out of both, and operations settles and controls whatever the others initiate.

Cash and Liquidity

At the core of the mandate sits a single requirement: the firm must be able to meet its obligations as they fall due. That is liquidity, and it is not solvency — a firm whose assets exceed its liabilities is solvent, yet a solvent firm still fails if it cannot produce cash in the currency and at the moment an obligation requires it. Treasury manages the first condition directly. The domain covers visibility of the cash position across the firm’s accounts and entities, forecasting the inbound and outbound flows that move it, mobilizing cash to where an obligation will land, covering shortfalls before they bind, and placing surplus so it earns a return without compromising access.

The operating mechanics — how cash is concentrated across accounts, how positions pool across entities, how forecasts are built and reconciled against actuals — belong to liquidity coordination. The mandate fixes the one thing the firm cannot leave unowned. When an obligation comes due and the cash is not there, the failure lands on treasury, whatever the operating reason behind it.

Funding and Capital-Structure Execution

Treasury secures and maintains the firm’s access to capital and executes the capital-structure decisions taken above the function. Day to day the work is concrete. Treasury maintains the funding stack — committed revolving credit facilities, uncommitted bank lines, commercial paper programs, term debt and bond issuance — manages the maturity profile so refinancing does not cluster or fall due into a weak market, draws and repays against facilities as the position requires, and runs the operational mechanics of an issuance, from arranger coordination to settlement of proceeds.

The decision this executes against is not treasury’s: the leverage target, distribution policy, and which obligations get funded sit with capital allocation. Treasury reports what funding is feasible and at what cost, then executes the chosen path. This domain interlocks with cash and liquidity at a specific point — undrawn committed facilities are contingent liquidity, a backstop the firm can draw when operating cash falls short — so funding capacity is itself a liquidity reserve, and treasury manages the two together because each one’s slack is the other’s backstop.

Financial Risk

Operating and carrying a capital structure generate market and counterparty exposures as a by-product, and the mandate is to hold those exposures within a defined tolerance rather than to eliminate them. The exposures fall into recognizable classes: currency risk on cross-border revenue, costs, and balances; interest-rate risk on floating-rate debt and on reinvested cash; counterparty and credit risk, including concentration on the banks that hold the firm’s cash and on the counterparties to its hedges; and liquidity risk, which overlaps the first domain.

What bounds this domain is the line between financial risk and operational risk. A currency movement or a counterparty default is financial risk and sits with treasury; a failed payment, a control breakdown, or a fraudulent disbursement is operational risk and sits with treasury operations and control. The distinction matters because the two are managed with different instruments — exposure limits and hedges on one side, segregation and authorization controls on the other — and conflating them leaves gaps in both.

Treasury Operations and Control

The fourth domain is the processing, settlement, and control apparatus that executes and verifies everything the other three initiate — the back and middle office of the function. Treasury operations conventionally divides into three roles held apart from one another. The front office initiates: it deals, funds, invests, and executes hedges — the action arms of the first three domains. The middle office measures and controls: it values positions, monitors exposures against limits, and checks compliance with policy. The back office settles and reconciles: it confirms deals, processes and releases payments, manages the bank account estate, and reconciles treasury’s records against the bank and the ledger.

The separation between these roles is itself the primary control. The desk that strikes a deal does not confirm and settle it; the person who initiates a payment does not release it alone. Segregation of duties and four-eyes release live here, and this domain owns the operational risk the other three generate when their actions are processed. The machinery through which the work runs — account architecture, bank connectivity, the treasury and ledger systems, payment execution — is the operating architecture of the function; the control mechanisms that govern it belong to internal financial controls, authorization structures, and delegated authority. This domain owns the integrity of execution itself. A deal is not done until it is confirmed and settled; a payment is not released except under four-eyes control; a balance is not trusted until it reconciles against the bank and the ledger. Whatever operational failure the other three domains throw off is meant to surface here, before money leaves the firm.

Taken together, the four domains parcel the function into clear lines of responsibility — one answerable for the cash position, one for funding access, one for exposures held within tolerance, one for processing and control. When something breaks, it breaks inside a domain with a named owner, not in the gaps between them.

The Operating Architecture

A forecast is worth nothing if the cash position feeding it is assembled by hand from a dozen bank portals, and a control is worth nothing if a payment can leave outside the channel that enforces it. Both failures trace to the same layer: the stack through which treasury sees and moves money — the accounts the firm holds, the channels connecting those accounts to its systems, the systems holding the position of record, and the apparatus that originates payments. The mandate’s three substantive domains — liquidity, funding, risk — run only as well as this stack lets them; get it wrong and all three underperform no matter how sound the policy above them is.

Bank Account Architecture

The firm holds accounts in a structure, not a flat list. A typical estate organizes around header or concentration accounts into which subsidiary balances sweep, with operating sub-accounts beneath them by entity, currency, and purpose. Concentration and pooling — run by liquidity coordination — operate on the account hierarchy treasury defines here; without that hierarchy, idle balances cannot be mobilized at all. A poorly structured estate strands cash: balances sit in accounts no sweep reaches, and the firm funds a shortfall in one entity while idle cash sits in another.

Every physical account, though, carries a cost. Each one is a KYC and mandate-maintenance obligation with its bank, a reconciliation surface that has to be tied out, and a place cash can sit trapped, so treasury actively rationalizes the estate and resists letting it grow. Two mechanisms do the rationalizing. Bank account management — increasingly electronic (eBAM), using the ISO 20022 acmt message family to standardize opening, closing, and mandate changes between corporate and bank — manages the estate as a controlled inventory, not a sprawl of separately negotiated relationships, though eBAM adoption across banks remains uneven. Virtual accounts collapse the physical count directly: a bank issues virtual IBANs that sit under one physical account, and incoming funds addressed to a virtual IBAN are attributed automatically to the payer, customer, or subsidiary it represents. This auto-attribution is what makes collections-on-behalf-of workable and reconciles receivables on arrival, while replacing dozens of physical accounts with one — fewer accounts to open, KYC, fund, and reconcile.

Bank Connectivity and Messaging

Connectivity is the pipe over which the firm’s systems exchange instructions and information with its banks, and the channel chosen is consequential: it fixes integration cost, how many banks the firm reaches through one connection, and whether treasury is locked into each bank’s proprietary portal — manual, un-automatable, and a single point of operational dependence.

| Channel | What it is | Where it fits |

|---|---|---|

| Host-to-host | Direct system-to-system file exchange (typically SFTP), carrying ISO 20022 XML or legacy formats (BAI2, MT940) | High-volume automated flows with a primary bank; set up bilaterally, per bank |

| SWIFT for Corporates (SCORE) | One connection to the SWIFT network reaching many banks under a single standardized channel | Multi-banked firms wanting one pipe instead of one integration per bank |

| EBICS | Bank-transmission standard used across Germany, France, Switzerland, Austria | European footprint where EBICS is the regional norm |

| Bank / open-banking APIs | Real-time request-response over bank or PSD2 APIs | Intraday balance polling, instant payments, embedded flows; bank coverage still uneven |

Over those channels rides a message layer, and ISO 20022 is what lets one treasury system talk to many banks without maintaining a separate format per bank. Outbound, the firm sends pain.001 to initiate a credit transfer and receives pain.002 as the status report telling it whether the instruction was accepted, rejected, or is pending — the difference between believing a payment went out and knowing it did. Inbound, camt.053 is the end-of-day statement that accounting reconciles to, camt.052 is the intraday report treasury reads its live position from, and camt.054 notifies individual debits and credits. The cross-border network’s own migration to ISO 20022 under CBPR+ has now run through its MT–MX coexistence window, so the proprietary and legacy formats that once fragmented bank connectivity are converging on one standard. For a multi-banked treasury that means retiring per-bank portals and running one connection that speaks one message set — the difference between a payment run touched by hand at four banks and one released straight through.

The TMS and ERP Layer

Two systems hold the data the function runs on, and where the cash position of record lives between them shapes the whole architecture. The ERP holds the sub-ledger and general ledger — what has been booked. The treasury management system holds the live cash position, deal and instrument records, exposures, and the bank-connectivity layer — what is happening now and what is at risk. Firms resolve the split two ways. Some run treasury inside the ERP’s own modules — SAP Treasury and Risk Management within S/4HANA, or Oracle’s treasury functionality — gaining native integration with the ledger at the cost of depth in treasury-specific function and multi-bank reach. Others run a best-of-breed TMS — Kyriba, FIS, ION Treasury, GTreasury, Coupa Treasury, Serrala — gaining depth and broad bank connectivity at the cost of a TMS-to-ERP integration that has to be built and maintained.

That integration is not incidental; it is the reconciliation seam from the function’s boundary, instantiated in systems. A payment released in the TMS has to book in the ERP’s ledger, and a balance reconciled in the ERP has to match the position the TMS manages. When the two drift — a payment released but not booked, a statement reconciled in one system and not the other — the firm holds two cash figures that disagree, and the discipline of keeping them tied out is what financial reconciliation architecture governs. When the TMS release record and the ERP posting stop matching the bank statement, treasury loses its authoritative position; the control is a daily break-and-clear routine with named ownership, run before the position is published each morning.

Payment Execution Architecture

How payments originate and from which entity is an architectural choice with direct consequences for control, account count, and intercompany complexity. The baseline pattern is the payment factory — a single hub that receives payment requests from across the firm, standardizes them into one outbound flow (one pain.001 stream, one set of bank connections), and applies release controls in one place. Centralizing this way collapses dozens of separately controlled payment paths into a single governed channel, with fewer connections to maintain and one point at which authorization and segregation apply.

Two structures sit on top of the factory. Payments-on-behalf-of (POBO) has a central entity pay vendors on behalf of operating subsidiaries: the subsidiary’s payable is settled from the central entity’s account, which collapses the subsidiaries’ external payment accounts but creates an intercompany position — the central entity is now owed by the subsidiary it paid for — that has to be tracked and settled. Collections-on-behalf-of (COBO) is the mirror, and it depends on the virtual accounts described above to attribute each incoming payment to the subsidiary it belongs to. Taken to its conclusion, the structure becomes an in-house bank: central treasury runs internal current accounts for subsidiaries, funds them internally, and executes their FX internally, so the subsidiaries bank with treasury rather than (or alongside) external banks. The in-house bank internalizes flows that would otherwise cross external rails, concentrates liquidity, and strips out external accounts and external FX cost — but it makes central treasury a critical node whose failure or misreconciliation propagates to every entity that banks through it, which is why the structure is treated as part of the firm’s multi-entity infrastructure rather than a local convenience.

Across all four layers the same trade recurs: each consolidation that buys efficiency — fewer accounts, one position of record, one payment channel, one internal bank — concentrates dependence in the same motion. The operating stack is therefore built by weighing account sprawl and manual handling against single points of failure, and where a given firm draws that line is a design decision, not a default.

Cash, Liquidity, and Funding in Operation

Day to day, the mandate’s three substantive domains collapse into one continuous operation: read the position, fund the gap, place the surplus, and do it again. Effectiveness shows in the daily rhythm that runs these domains against the firm’s real flows, not in the policy that defines them.

The cycle begins with the cash position. Each morning treasury pulls intraday balances across the account estate — the camt.052 reports described above, or API polling where the bank supports it — nets them against the flows known to land that day, and produces a position by currency and by entity: how much cash the firm holds, where it sits, and what is moving. Every funding and investment decision that day runs off this number. Get it wrong and the decisions are made blind, and blindness costs in both directions — idle cash left unremunerated when it cannot be seen, a coming shortfall covered late at an overdraft rate the firm would not have paid with a day’s notice.

If the position is the present, the forecast is the near future — and it drives the decisions that cannot wait for the flow to arrive. Treasury runs a layered forecast: a short flow-based view over days and weeks that sizes today’s funding and investment, and a longer view that sizes facilities and refinancing, each reconciled against actuals to calibrate it. Forecast error costs asymmetrically. Under-forecast the cash that will arrive and the firm carries an excess buffer earning less than its cost of capital; over-forecast it and the firm comes up short, drawing emergency funding or running into overdraft at a penal rate. The mechanics of building the forecast and reconciling it against actuals belong to liquidity coordination. What matters at the level of the function is that the forecast is the decision input, and its accuracy sets the floor on how tightly the firm can run its cash.

Knowing the position is not the same as being able to use it. Cash mobilization moves funds to where an obligation will land — across accounts, entities, and currencies — and runs into constraints a balance sheet never shows. Cash can be trapped: capital controls, withholding rules, and sub-custody arrangements hold a balance inside a jurisdiction or entity, so the firm funds a shortfall in one place while idle cash sits unreachable in another. Moving across currencies adds an FX cost and an execution step. Timing binds on its own. What sets when cash actually leaves and arrives is the payment’s value date, not the moment it was initiated. Originate a transfer after a rail’s cut-off, or into a weekend or holiday with no settlement cycle, and the funds lock until the next cycle clears — working capital tied up for days on nothing but calendar mechanics. The per-instruction settlement behaviour behind this belongs to the payment and settlement systems; the cross-account movement mechanics belong to liquidity coordination. At the function level, mobilization is the discipline of getting usable cash to the point of need before the need binds.

A short position gets covered from a graded set of sources, cheapest and most deliberate first. Treasury draws against a committed revolving facility, issues or rolls commercial paper, and only at the margin runs into intraday or overdraft lines — the most expensive sources and the ones least intended to bear load. Here the liquidity and funding domains interlock in practice. An undrawn committed facility is contingent liquidity, a reserve convertible to cash on demand, so the daily covering decision is made against the funding stack, not in isolation from it, and a facility’s headroom reads as part of the liquidity position.

A long position has to be placed, and treasury places it under a capital-preservation mandate, not an investment one. The objective order is fixed and runs in one direction: security of principal first, then liquidity — access to the cash on the date the forecast says it is needed — and only then yield, which is whatever the first two leave room for, never the thing being maximized. The investment policy turns that order into constraints. It limits what surplus cash may be held in, typically money market funds, bank deposits, Treasury bills, repo, and high-grade short paper. It sets counterparty and concentration limits, so that placing cash does not quietly rebuild the bank-concentration risk treasury is there to manage. And it caps tenor against the forecast, so cash is never locked past the date an obligation will claim it. The instruments themselves, and how a reserve is composed across them, are covered on the reserve-asset pages. The framework here is descriptive: it states the constraints surplus is held under and treats any modelling of placement as computation under the firm’s own policy — never as a recommendation to hold one instrument over another.

Underneath all of this, funding execution runs continuously and closes the loop. Treasury draws and repays against facilities as the position swings, rolls commercial paper as it matures, and matches the tenor of funding to the horizon of the forecast — keeping maturities from clustering or falling due into a market the firm would rather not refinance into. The capital-structure decisions this serves are taken above the function. The daily work of keeping the firm funded against them is treasury’s, and it is the same loop — position, gap, surplus — turned over again every day.

Financial Risk Management

Operating across currencies, carrying a capital structure, and holding cash with counterparties throws off market and counterparty exposures as a by-product — these are the financial risks treasury manages. The mandate set the boundary, financial risk and not operational risk, and named the classes; what follows is how each is held within tolerance in practice. One operational spine runs through all four. A risk that is not measured cannot be managed, so each class starts with exposure capture from the same position, forecast, and ERP feeds that drive the cash cycle, then nets the exposure down before acting on it, then acts only within a defined limit. The job is not to remove these exposures but to size them and bound them, holding them inside the tolerance policy sets.

Currency risk splits into three exposures, and they are not managed alike. Transaction exposure — committed and forecast cash flows in a foreign currency — is the one treasury hedges actively, because it converts directly into cash gained or lost. Translation exposure arises when foreign-entity balance sheets consolidate into the reporting currency; it is an accounting effect that moves no cash, and it is hedged selectively if at all. Economic exposure, the competitive effect of currency moves on the business, is rarely hedged operationally. On transaction exposure the mechanics run capture, net, hedge. Treasury pulls the exposures by currency from the forecast and nets long against short across entities first. That netting matters. Intercompany netting strips out offsetting positions, so the firm hedges the residual rather than the gross and pays the spread once, on the net. Only then does it hedge the net — with forwards, currency swaps, or options. Hedge accounting decides whether the hedge’s gain or loss lands in the same period as the item it hedges. Designation under IFRS 9 or ASC 815 aligns that timing and stops a hedge that economically reduces volatility from manufacturing earnings volatility instead — at the cost of real documentation and effectiveness-testing discipline. Two breaks recur: hedging gross instead of net, and hedging a forecast exposure that never materializes, which leaves a derivative with no underlying — a naked position created by the act of hedging.

Interest-rate risk sits on two sides that partly offset: floating-rate debt, whose cost rises with rates, and reinvested cash, whose return rises with them, so a firm with both carries a smaller net exposure than either leg alone. The reference framework is now the risk-free-rate world that replaced LIBOR — SOFR in USD, SONIA in GBP, €STR in EUR, with TONA and SARON regionally — and the floating book is read off those benchmarks. Treasury measures the net floating exposure and hedges it with interest-rate swaps (paying fixed, receiving floating) or caps where the firm wants protection without giving up the downside. The fixed-to-floating mix of the debt stack is a capital-structure decision taken above the function; treasury executes it and hedges the residual. The break to watch is basis risk — a hedge referenced to one rate against debt referenced to another leaves a gap that widens exactly when rates move — and, again, over-hedging the debt side while ignoring the natural offset the cash side provides.

Counterparty and credit risk has two faces, and the second is the one corporates underestimate. The first is conventional: the counterparties to the firm’s hedges, deposits, and investments can default, managed through counterparty limits graded by rating, collateral and CSAs on derivative exposures, and monitoring of ratings and CDS spreads as early signals. The second is concentration on the banks that hold the firm’s operating cash — long treated as an operational convenience rather than a credit exposure, until it is one. The Silicon Valley Bank failure in March 2023 made the point concretely. Firms holding their operating cash concentrated at a single bank, much of it above the $250,000 FDIC insurance limit, saw their entire transactional balance frozen overnight and could not make payroll. An uninsured deposit is an unsecured claim on the bank, not cash the firm simply holds. The response treasury takes from this is to treat operating-cash concentration as a counterparty exposure in its own right — spreading transactional cash across banks and sweeping surplus into instruments held away from the transactional bank. That loops straight back to the placement discipline of the cash cycle: the concentration limits on surplus investment exist precisely so that placing cash does not quietly rebuild the bank exposure the firm just diversified out of.

Liquidity risk overlaps the cash-and-liquidity domain, but framed as an exposure it is the risk that the firm cannot raise cash when an obligation requires it — either because an asset cannot be sold without loss (market liquidity) or because funding cannot be drawn or rolled (funding liquidity). Managing it has four moving parts. Treasury holds a liquidity buffer of committed undrawn facilities plus high-quality liquid placements, staggers funding maturities so refinancing does not cluster, and stress-tests the position against a shortfall scenario. It also watches covenant headroom, because a breach can trigger acceleration and turn a manageable position acute overnight. The breaks here are specific: relying on uncommitted lines a bank can pull at the moment they are needed; clustering maturities into a single refinancing window; and counting on contingent liquidity that evaporates under the same stress that creates the need — a backstop from a bank itself under pressure is correlated with the event it is meant to cover.

All four stay financial risks, held within tolerance rather than eliminated. The moment one shades into operational risk — a payment that fails or is fraudulently induced, a reconciliation that will not tie out, a control quietly bypassed — the instruments change hands — limits and hedges give way to segregation, authorization, and the control surface, and the exposure stops reading as a market move and starts reading as money gone or a balance no one can trust. That is the territory where the function actually breaks.

How the Function Is Organized

Everything described so far — the mandate, the operating architecture, the daily cycle — can be built in materially different shapes, and the shape changes how the function behaves. Three structural axes determine it. They are largely independent of one another but decided together: how far treasury authority and cash concentrate at the group center, which parts of the machinery the firm runs itself, and how the structure maps onto the firm’s legal entities. Each is a decision with operational consequences, and each has its own detailed treatment; here they are placed and their trade-offs named.

Centralization sets the first axis — how far position-keeping, funding, FX execution, and payment release concentrate at a single group function rather than sit with regional or entity-level treasuries. Pull those activities to the center and cash visibility is maximized, pooling and netting reach across the whole firm, and scarce treasury expertise concentrates where it earns its keep. It costs the firm distance from local knowledge — local banking relationships, the tax and regulatory nuance of each jurisdiction — and it concentrates failure in one place; when the central function goes down, every entity that depends on it goes down with it. Leave cash and decisions with the entities and the opposite holds, with local responsiveness preserved but visibility fragmented and group-level pooling out of reach. Most large firms land on a hybrid, centralizing policy, position-keeping, and funding while delegating local execution inside group limits; where the line falls is the substance of centralized-versus-decentralized treasury models. What the axis fixes, for the function, is where the cash position is assembled, how far pooling can reach, and where payment authority is exercised — the givens the operating architecture and the daily cycle build on. And it is realized through delegation. The centralization choice becomes a delegated-authority structure that sets what an entity may do without group sign-off and which actions escalate; the position on this axis and the authorization structures that express it move together, tightening or loosening the control surface as one.

Sourcing sets the second axis — which parts of the function the firm runs itself and which it hands to a third party such as a bank, a managed-service provider, or a back-office outsourcer. At one end the firm is fully in-house, operating its own TMS, bank connectivity, and operations team. In the middle a bank runs pooling and sweeping on its behalf, or a provider handles payment runs and reconciliation. At the far end the firm leans on a banking partner for most of the operating layer. This choice trades control and capability against fixed cost and dependence. Running in-house keeps control over the position, the controls, and the data, but it demands the systems and connectivity to do the work — and a team able to maintain both, a fixed cost a smaller firm cannot justify against its volume. Delegating converts that to variable cost and buys a provider’s scale, at the price of visibility into how the work is done and a continuity dependence on the provider. The full comparison sits with in-house-versus-external financial operations. What holds at the function level is that a delegated activity is still treasury’s risk. Outsourcing the processing does not outsource the consequence of its failure, so a provider running part of the operating layer becomes a counterparty and continuity exposure the function manages, not a piece of the firm it has stopped thinking about.

The third axis bites the moment the firm is more than one legal entity, shaping how the account, connectivity, and intercompany structure maps onto the legal-entity map. A firm with subsidiaries across several currencies and jurisdictions has to decide how accounts sit across entities, how connectivity reaches each one, and how the pooling, POBO/COBO, and in-house-bank structures from the operating architecture overlay the legal structure. It is a distinct axis because every cross-entity cash movement is also an intercompany transaction, carrying tax, transfer-pricing, and entity-solvency consequences a single-entity firm never meets. Concentrate cash through pooling or an in-house bank and the move creates intercompany positions that have to be documented and priced — transfer pricing applies to intercompany funding and to the in-house bank’s internal rates — and held inside each entity’s own solvency and thin-capitalization limits. Where this bites is concrete. A sweep that would pull a subsidiary’s surplus to the center can be blocked outright by local thin-capitalization rules, or taxed through a withholding charge on the intercompany loan it implies, so the most cash-efficient structure is sometimes simply unavailable and treasury builds to the constraint, not around it. The structural substrate that carries all of this is the subject of infrastructure in multi-entity organizations.

The three axes resolve together, not in sequence. A centralized in-house bank cannot run unless the firm also commits to operating in-house the connectivity and systems it depends on; a decision to outsource the operating layer caps how centralized the firm can be, because it inherits the provider’s structure; and both sit inside whatever the legal-entity map allows. The organizational shape of the function is the simultaneous answer to all three, and that answer is what determines how the mandate, the architecture, and the daily cycle actually run at a given firm. A shape that is wrong for the firm — too centralized for its need of local knowledge, too outsourced for its control requirements, built against its entity constraints — rarely fails outright. It underperforms quietly. Cash that could be pooled sits stranded, a control the firm believes it has actually lives with a provider, and a structure that looks optimal on paper gets throttled by a tax rule. The damage shows up later, as the function operates, never at the organizing decision itself.

Failure Modes

Sitting at the center of the firm’s financial operating system, the treasury function has failures that rarely stay where they start. A wrong position, a payment that should not have left, a balance that cannot be reached — each originates inside the function and surfaces downstream: in a plan built on a number that was never real, a loss the control surface should have caught, a payment the firm was solvent enough to make and still missed. They sort into three classes by the capability each destroys — visibility into the position, control over what leaves, and access to cash that is real and seen but unusable. Operationally the split matters because each class is caught by a different instrument and travels a different path.

Visibility failures corrupt the position the rest of the firm acts on, and the three mechanisms that produce them compound. Forecast error misstates the cash that will arrive. Under-forecast it and the firm carries an idle buffer earning below its cost of capital; over-forecast it and the firm covers a shortfall late at a penal rate. Because every funding and investment decision that day runs off the forecast, one bad number propagates into all of them. Account sprawl degrades the position at its source. An estate grown faster than it was rationalized leaves balances in accounts no sweep reaches and no morning pull captures, so the position is assembled from an incomplete picture, and the firm funds a gap in one entity while idle cash sits unseen in another. Worst of the three is the reconciliation gap, because it removes the firm’s ability to say which number is true. When treasury’s managed position, the ERP’s booked balance, and the bank statement stop tying out — a payment released and not booked, a statement cleared in one system and not the other — the firm holds two or three cash figures that disagree, with no authoritative one among them. Closing that gap is what financial reconciliation architecture governs; its absence is where the most expensive surprises incubate, since a break left unreconciled stays invisible until it is large. The 2024 collapse of the banking-as-a-service provider Synapse ran on exactly this, at scale. The ledger recording what end-users were owed and the partner banks’ records of the pooled accounts holding the cash could not be reconciled. A shortfall opened between the two, and with nothing authoritative to adjudicate it, end-users’ operating balances froze while the records were litigated. The mechanism generalizes. When the record of cash and the cash itself diverge and nothing can settle which is right, the cash is unusable whether or not it exists.

Control failures let money leave the firm wrongly, and they realize as a direct, often unrecoverable loss rather than a mismeasurement. The characteristic mode is fraudulent payment induction — business email compromise, where an attacker impersonating a senior executive or a known supplier gets a legitimately authorized operator to originate a payment to an attacker-controlled account. What makes it dangerous is that it breaks no system. The payment is correctly formatted, validly authorized, and released through the proper channel, so every technical control passes and the fraud rides on the human authorization rather than circumventing it. The defenses are procedural and sit outside treasury’s own machinery — callback verification on payee changes, segregation of duties so initiation and release rest with different people, four-eyes release above a threshold, and dual control on changes to the payee master. This is why the mode is governed by internal financial controls, authorization and approval structures, and the delegated-authority structure that defines who may release what. The same class covers the slower failure of segregation eroding over time — release rights granted for convenience, a four-eyes step waived under deadline, a payee change made without dual control. External attacker or internal drift, the consequence is identical. Cash leaves on a validly released instruction; because it was authorized, recovering it means catching it before settlement finality, past which the funds are gone.

Access failures are the case where the cash is real, the position is correct, and the firm still cannot use the money when an obligation requires it — a solvent firm missing a payment on mechanics alone. Three mechanisms produce it. Cash gets trapped by capital controls, withholding rules, or sub-custody arrangements that hold a balance inside a jurisdiction or entity, so a group-level figure overstates what is actually deployable to the point of need. Value-date timing locks cash on the calendar. A transfer originated after a rail’s cut-off, or into a weekend or holiday with no settlement cycle, does not clear until the next one — working capital tied up for days on the gap between initiation and value date. (The per-rail behaviour behind this sits with the payment and settlement systems.) Bank concentration converts a counterparty event into an access failure outright. Cash concentrated at a single bank that fails freezes as an unsecured claim — the March 2023 Silicon Valley Bank failure again, where firms holding their transactional balances at one bank, much of it above the deposit-insurance limit, could not make payroll though they were solvent and the cash existed. None of these shows on the balance sheet, which records the cash as held. Reachability is what fails here, and it is caught only by managing the position for usable cash at the point of need — not by watching an aggregate balance that says the money is there.

One property runs through all three classes: in a central node, a local failure becomes a system failure. A forecast error is one number wrong, until every funding and investment decision built on it is wrong too. A reconciliation break is one unexplained difference, until it is a balance no one can trust. A trapped balance is one account, until it is the account that was meant to make payroll. The treasury function touches liquidity coordination, settlement, reconciliation, and the multi-entity structure, so a break that starts as a single mispriced position or a single un-reconciled account does not stay contained — it arrives, eventually, as a payment the firm cannot make on a day it cannot move.